India’s Emerging Upstream EV Battery Ecosystem | Whitepaper Excerpt

Excerpt reproduced from “The Battery Imperative: Global Lessons for India’s EV Battery Ecosystem“ by Deloitte. Whitepaper released at EVreporter ELECTRICON 2026 on May 22, 2026, where Deloitte participated as the event’s Knowledge Partner.

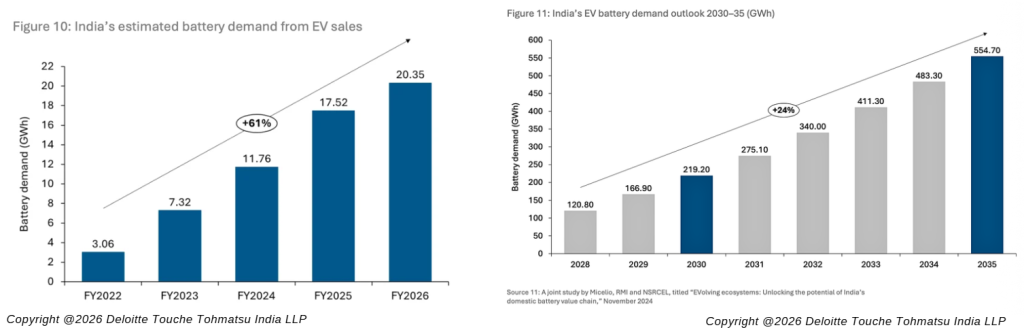

FY2026 was a strong year for India’s automotive industry, with auto retail reaching a historic high of ~2,96,71,000 units. EV sales experienced a similar boost, reaching ~25,16,000 units with a YoY growth of 24.2 percent, a significantly higher figure than the 15.3 percent YoY growth recorded between FY2024 and FY2025. Battery demand was driven by the e-4W and large-form-factor segments: e-car sales nearly doubled from FY2025 to FY2026, whereas e-bus sales increased by 50 percent and e-truck sales rose by 2.5x.

LFP remains the battery chemistry of choice across EV segments, except for electric two-wheelers. LFP batteries are favoured for heavy-duty applications such as long-range buses and commercial vehicles up to the largest 55-tonne GVW category. As India’s EV industry matures, adoption is expected to accelerate. Based on a study, India’s EV demand is expected to reach ~219 GWh and ~555 GWh by 2030 and 2035, respectively.

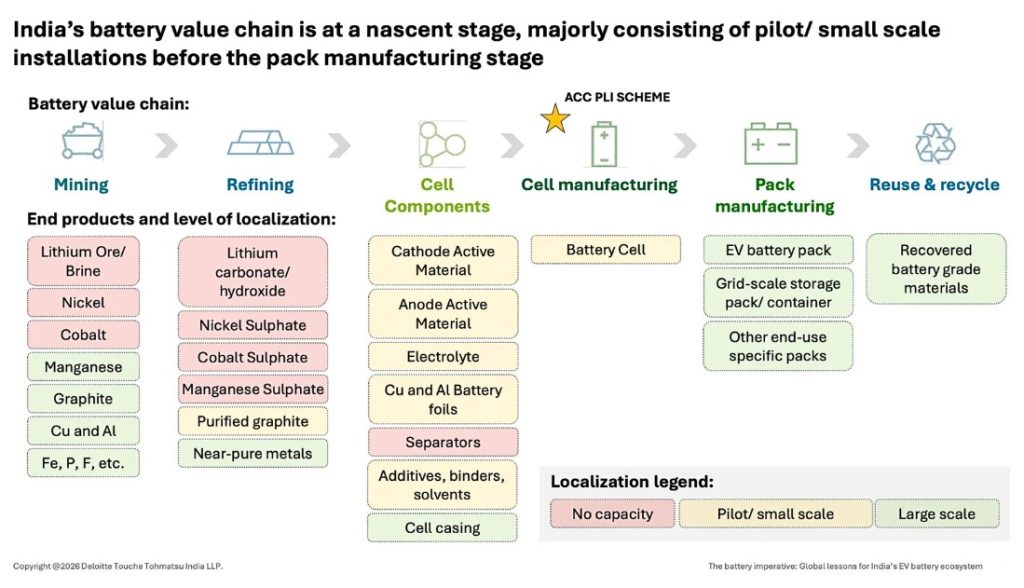

An overview of the Indian battery value chain

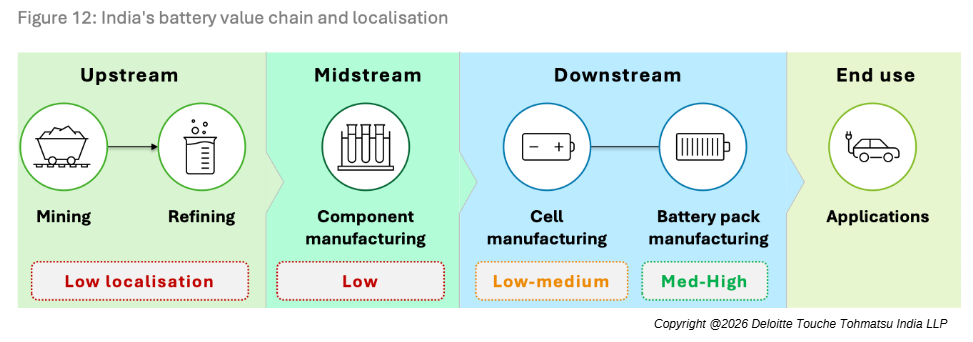

The battery demand is growing in India. Meeting it will require a robust domestic battery manufacturing ecosystem with capabilities across the entire value chain.

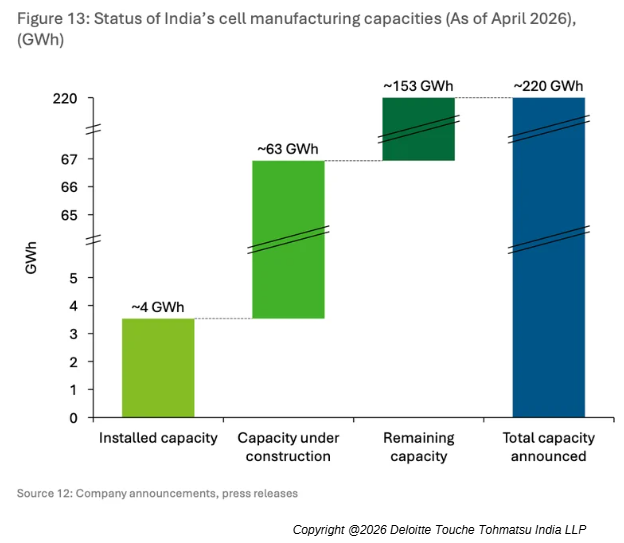

Cell manufacturing

Due to a supportive policy environment at both the central and state government levels, battery cell manufacturing in India is making steady progress.

The Production Linked Incentive (PLI) scheme has provided the necessary momentum, leading to the announcement of over 220 GWh of manufacturing capacity by more than 13 industry players (including 40 GWh allocated under the PLI ACC scheme.

The following are the key challenges faced by battery cell manufacturers:

- Currently, there is a high import dependence on plant and machinery. Equipment from China is facing delivery delays and uncertainty regarding export controls, while equipment options outside China are more expensive, which adds to the capital cost.

- In terms of operational cost, material costs are estimated to be 15–20 percent higher due to extreme import dependency. Materials typically account for roughly 70 percent of the total cell cost, translating into a significant disadvantage in the final cell price.

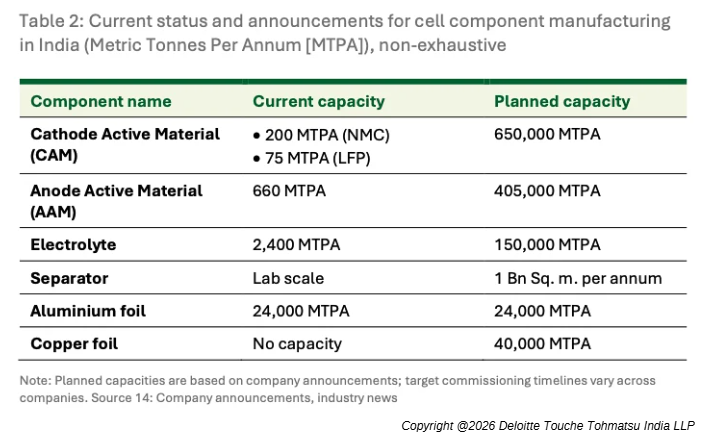

Component manufacturing

India is heavily dependent on imports for key cell components such as cathodes, anodes, electrolytes and foils to support its expanding ACC manufacturing, which creates significant exposure to global supply chain risks. In view of this supply chain gap, several companies have announced plans to localise component manufacturing. A few pilot-scale facilities for cathode active material, anode active material (natural and synthetic) and electrolytes are already operational. These announcements involve large-scale production to serve both domestic and overseas markets.

The following are the key challenges faced by the industry:

- Limited domestic precursor manufacturing (lithium carbonate/hydroxide, calcium carbide, etc.) results in high input raw- material costs.

- CAM and AAM manufacturing are energy-intensive processes, and the differential with subsidised tariffs available to Chinese players further increases the cost gap.

- Lengthy testing and qualification timeline; usually takes 12–18 months.

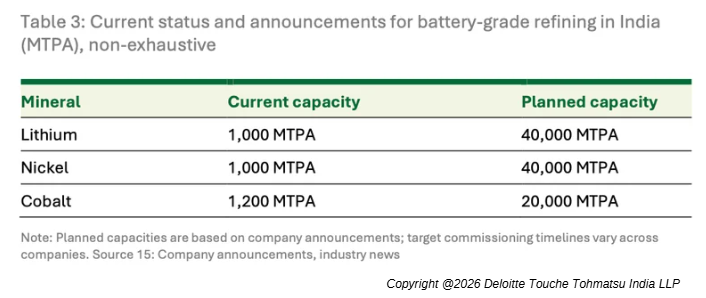

Refining

Refining involves processing mineral concentrates to achieve the purity and quality required for

battery-grade materials. This requires specialised chemical processes and high-quality feedstock. Due to stringent process requirements and an outsized environmental impact, battery-grade refining is even more geographically concentrated than component and cell manufacturing.

Certain Indian players are attempting to develop domestic refining capacities supported through foreign mineral assets and long-term supply agreements. For example, some Indian cathode active material manufacturers have forged strategic partnerships with players in South America and Africa to secure access to battery-critical minerals. Furthermore, a few anode players are pursuing collaborations with Indian oil Public Sector Undertakings (PSUs) to develop domestic needle coke manufacturing capacity, a precursor to graphite anode material.

The following are the key challenges faced by the industry players:

- The technical know-how for battery mineral refining is limited. Additionally, industry feedback suggests that technology licensing fees constitute a considerable portion of capex at the 5,000–10,000-tonne scale, thereby affecting project economics.

- The majority of technology providers are based in China, which imposed export controls on lithium refining technologies in July 2025, making access more difficult for Indian players.

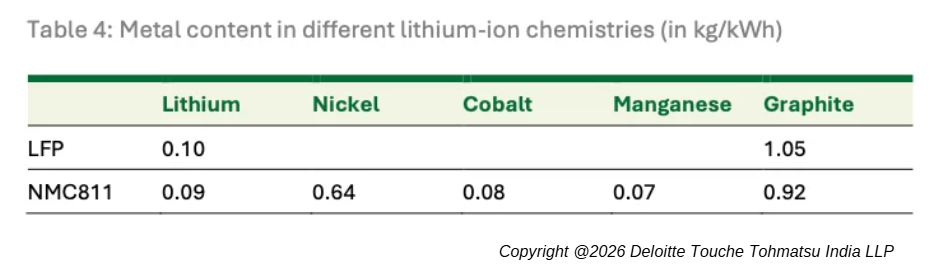

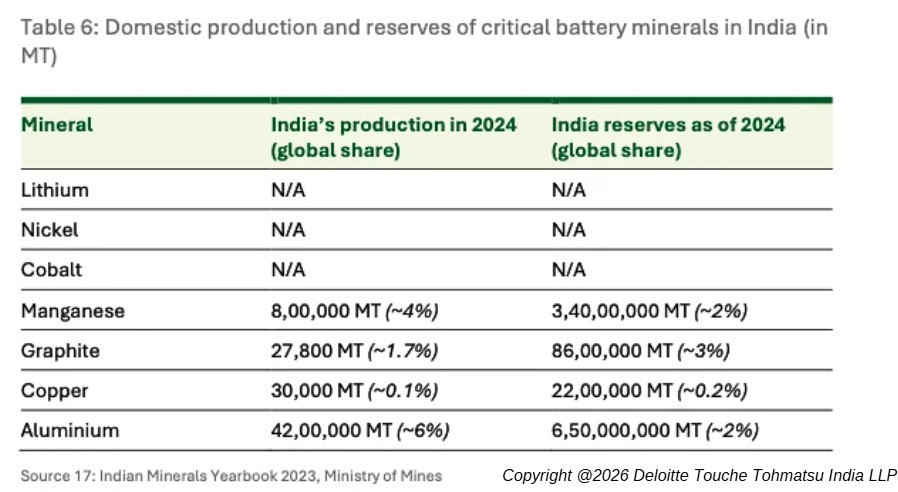

Mining

Lithium-ion batteries use several critical minerals for manufacturing. The mass of these minerals required for 1 kWh across various Li-ion chemistries is provided in the following table:

The global supply of lithium, nickel, cobalt, manganese and graphite is geographically concentrated, with China controlling significant portions of extraction capacity, followed by the Democratic Republic of Congo (DRC), Australia, South Africa and Indonesia.

India does not have commercially viable reserves of lithium, cobalt or nickel, but it does possess large deposits of manganese and natural graphite.

To secure the supply of critical raw materials for Indian industries, the government launched the National Critical Mineral Mission (NCMM) in 2025 with an allocation of ₹16,300 crore. The mission supports domestic and international mineral exploration, the acquisition of stakes in foreign assets, recycling, R&D, skilling and the development of a strategic stockpile of critical minerals. It also encourages PSUs to invest an additional ₹18,000 crore in critical mineral projects in collaboration with the private sector.

Takeaway

India’s EV battery market has now reached a scale where developing a domestic supply chain is both commercially viable and strategically important. However, the ecosystem is still at a nascent stage. While a large number of projects and capacities have been announced, only a limited number have progressed to actual implementation and commercial operations.

Any delay in execution could slow down the country’s ambition to become Aatmanirbhar in the battery manufacturing ecosystem and increase dependence on external supply chains. Coordinated efforts from both industry and government will be critical to build a robust, competitive and resilient domestic battery ecosystem.

Presented by

Anish Mandal

Partner, Deloitte Touche Tohmatsu India LLP

Contributors

Akshay Parihar, Associate Director

Raghav Rai Bhatnagar, Senior Consultant

Adarsh IR, Senior Consultant

Yash Pratap Singh, Senior Consultant

note: The complete whitepaper will be available on Deloitte’s website soon. The link to download will be shared in the EVreporter July 2026 magazine.

This article was first published in EVreporter June 2026 magazine.

Also read: Battery360 Alliance presents emerging battery technologies

Subscribe & Stay Informed

Subscribe today for free and stay on top of latest developments in EV domain.