Current LIB recycling landscape in India – leading players and commitments

The total demand for Lithium-ion Batteries (LiB) in India is expected to cross 230 GWh by 2030 from a mere ~5 GWh in 2020. The rising LIB is coupled with a need for a robust LiB recycling ecosystem primarily driven by the need to hedge

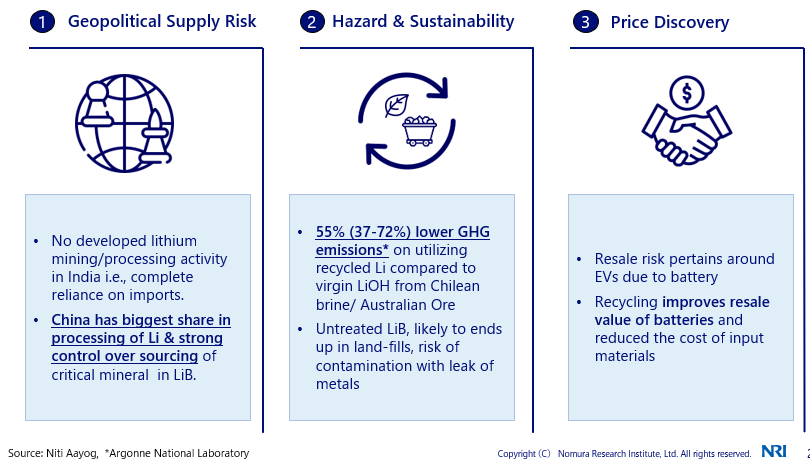

(1) geopolitical supply chain risk associated with critical minerals like lithium, cobalt and nickel in batteries,

(2) managing environmental hazards with untreated batteries and meeting sustainability goals with recycled material resulting in 55% GHG emission than using virgin materials from ores and

(3) improved price discovery for LiB batteries.

Considering Lithium alone, which is agnostic to the type of LiB chemistry, China currently has the dominant share (~70-80%) in processing and substantial control over sourcing with extensive contracts/deals, indicating concentration risk in the supply chain of Li. Even though India has now

allowed commercial mining of Lithium via “The Mines and Mineral (Development and Regulation) Amendment Bill 2023” and blocks of lithium ores are being placed under auction for further geological exploration, the development of a fully operational Li extraction and processing unit from these ores would take almost a decade. Thus, recycling lithium from imported batteries would be necessary to reduce the gap between local LiB demand and imports.

Overview of Battery Recycling Policy

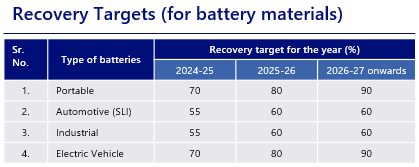

The policy impetus is to create a recycling ecosystem with “The Battery Waste Management Rules” with the latest amendments in 2023. The rules cover all entities ranging from producers, collection, segregation and treatment entities, refurbishes and recyclers. Apart from compliance with standards and registrations of recyclers with state pollution control boards, the policy also sets recovery targets for recyclers based on the type of battery.

The targets for recovery from LiB in electric vehicles are set to increase phase-wise from 70% in FY’25 to 90% in FY’27.

Image source: Nomura Research Institute

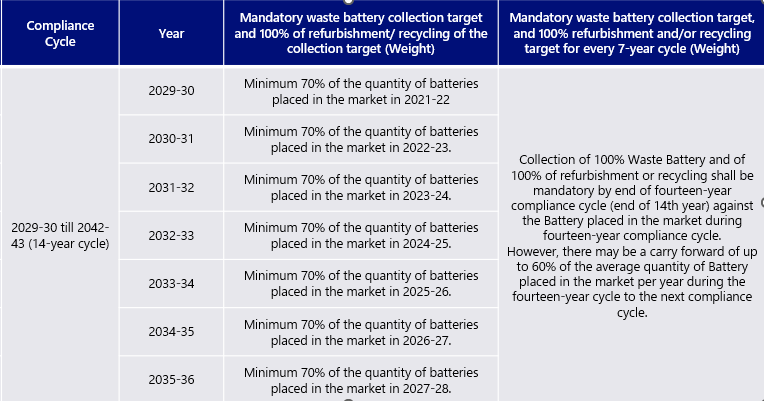

Rules also introduce Extended Producer Responsibility (EPR) targets for manufacturers and producers to be accountable for the collection, storage, transportation, recycling, and disposal of spent batteries. The targets push producers to have tie-ups with recyclers for compliance, allowing the development of the recycling ecosystem. However, there is scope in terms of having additional incentives for players with the capacity to recycle rather than mere trading of end-of-life (EoL) batteries, tighter registration norms of recyclers, and more substantial penalties for non-compliance.

EPR Targets in Passenger EVs| Image source: Nomura Research Institute

For 4W EV OEMs, 70% of the batteries introduced via vehicles in FY’23 are to be recovered in 2030-31 as per EPR targets. A detailed target is set against each year till 2035-36.

LiB Demand and Recycling Opportunity

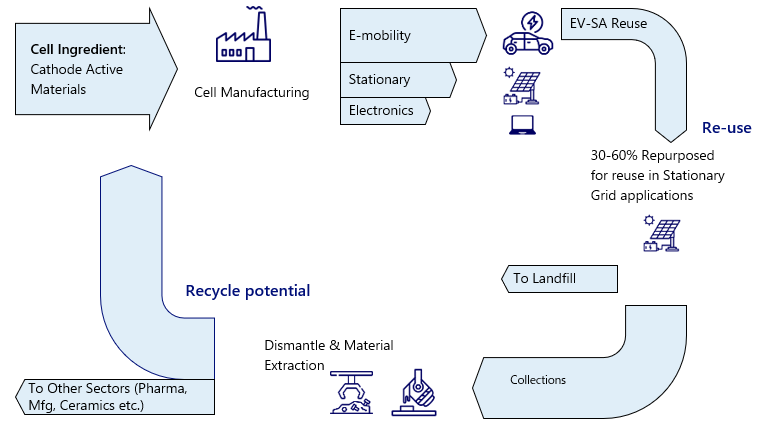

LIB Value chain | Image source: Nomura Research Institute

Stationary applications and EV batteries are the two applications that will consume most manufactured cells in the future. The cells entering into EVs are either repurposed or sent for recycling. Batteries used in large form factor vehicles like 4Ws and Buses are more suitable for repurposing than 2Ws and 3Ws. Niti Aayog estimates that only ~30% of the batteries used in 2Ws & 3Ws are ideal for repurposing, considering frequent usage cycles and chemistries. The number can be as high as 60% in the case of private 4Ws.

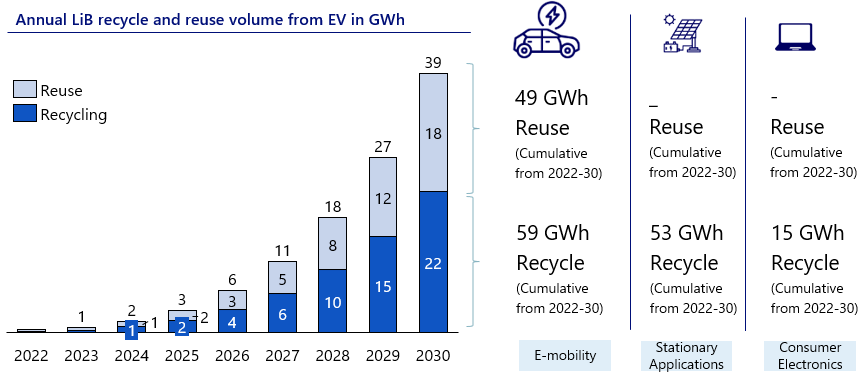

Annual LiB recycling and reuse volume in GWh | Image source: Nomura Research Institute

LiB Demand and Recycling Opportunity

The demand for stationary applications alone is expected to create a LiB demand of ~120-130 GWh in 2030, and ~15% of this demand in 2030 is expected to be met from re-purposed batteries obtained from EVs. Thus, re-purposing alone translates to an opportunity of ~18 GWh for EV recycling/repurposing players in 2030. Niti Aayog estimates that another 22 GWh is expected to add to the recycling potential, coming predominantly from stationary applications and remaining from EV batteries, which are not successfully re-purposed. Based on chemistries and cell form factors, the specific energy at the pack level today varies between 140-200 Wh/kg. With the given specific energy levels, an overall repurposing/recycling capacity of ~40 GWh in 2030 translates to 0.2-0.26 Million tons of annual capacity by 2030 for recycling/repurposing.

Key Players, Recycling Capacity and Outlook in India

Considering both black mass production and mineral extraction via hydrometallurgy/pyro-metallurgy, India has a capacity of 35,000 tons per annum (TPA) spread across players of processing LiB plants, of which ~10,000 is limited to only mechanical processing involving pre-treatment and shredding of batteries to produce black-mass. To meet the recycling/repurposing potential in 2030, the current capacity needs to be scaled by a factor of ~ 9X. Considering the global players, China has a total capacity of ~230,000 TPA in 2022, with a global capacity of around 0.4-0.45 Million TPA in 2022, i.e. India represents less than 5% of the global total in a rapidly evolving segment.

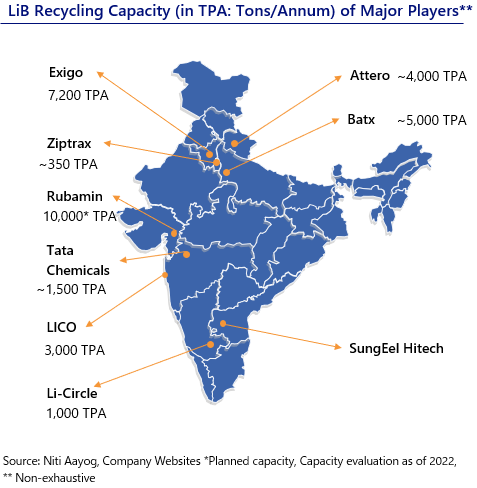

Currently, the recycling ecosystem in India has a healthy mix of start-ups, e-waste recyclers expanding horizontally and companies with an interest in battery materials or processing of critical battery minerals, including players like Lohum, Exigo, Ziptrax, Attero, Batx, Tata Chemicals, LICO, SungEel Hitech to name a few.

When it comes to technologies being adopted for extraction, hydrometallurgy is being adopted to a greater extent compared to pyro-metallurgy, considering that pyro-metallurgy needs higher throughput rates/volumes to justify the cost and is preferred globally by players with existing setups. In terms of capacity addition, select Indian players are expanding aggressively to match the 9X growth requirement for fully capturing the EV recycling/repurposing potential.

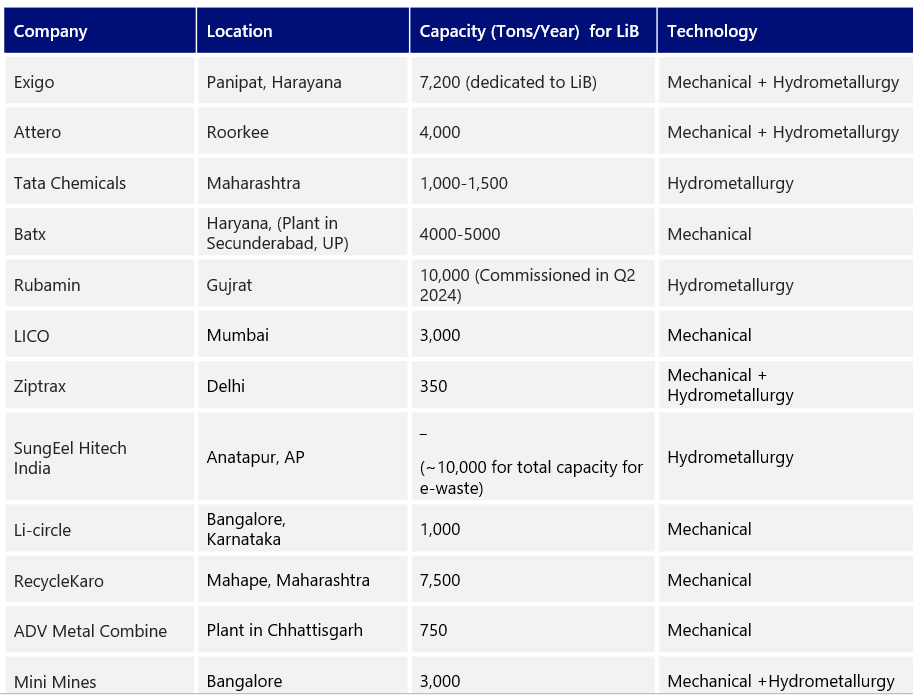

LiB Recycling Capacity of Major Players in India

- Exigo, with an existing capacity of 7,200 TPA, plans on expanding the capacity to 200,000 TPA. It has a higher preference for processing NMC chemistry and serves clients like Panasonic India and Samsung India.

- Attero, based out of Uttrakhand, plans to expand its capacity from 4,000 TPA to 19,500 TPA with an additional processing plant in Telangana.

- Rubamin, based out of Gujrat, conventionally had strength around processing contents of catalytic convertors and has expanded into LiB recycling with 10,000 TPA capacity utilising hydrometallurgy, which is expected to be operational in 2024. Rubamin has a capacity expansion plan of 30,000 TPA in phases.

- Lohum, with a large processing capacity of ~10,000 TPA, plans to expand to 50,000 by 2025. Lohum also has expansion plans outside India in UAE for a 3,000 TPA plant.

- LICO, based out of Mumbai, also plans to expand into hydrometallurgy-based extraction with a set-up of 10,000 TPA capacity from the current mechanical processing/black mass production capacity of 3,000 TPA.

- SungEel Hitech India, a subsidiary of South Korea-based SungEel, also has plants in Telangana to process 10,000 TPA of e-waste.

- Mini-mines is a start-up from Bangalore that is working on utilising hybrid hydrometallurgy technology for the extraction of battery materials.

With the rising number of players in the LiB ecosystem, there is also a rise in the strategic collaborations between OEMs and battery manufacturers, which would be necessary for growth considering evolving LiB chemistries, increasing complexities in the battery pack structure, and safety aspects of reverse logistics.

Govt incentives like PLI, which is currently targeted towards manufacturing advanced cell chemistries, if extended to recyclers with capabilities around hydro/pyro-metallurgy technologies, would enhance the localisation of the LiB value chain.

LiB Recycling Capacity of Major Players in India

Author credit:

Preetesh Singh, Specialist, CASE and Alternate Powertrains, Nomura Research Institute | preetesh.singh@nri.com

Athul Nambolan, Management Consultant, Nomura Research Institute

athul.nambolan@nri.com

Nomura Research Institute is a Global Think Tank and the Largest Consulting Firm in Japan. Established in 1965, it now has 24 Global Offices in 13 Countries with more than 10,000 employees.

Also read: Lithium-ion cell manufacturing and value chain | Current landscape in India

Subscribe & Stay Informed

Subscribe today for free and stay on top of latest developments in EV domain.