Market growth through original spare parts availability and the role of independent service points

Objective of the Paper:

1. Leveraging Independent Service Points, 2nd Sales Market Technicians and Roadside Mechanics.

2. Positive Impact of Easy Availability of Original Spares in the open market through Distributor Network.

Scope of Discussion: Sub Premium Cars only, Compact Segment cars.

Out of Scope : Premium and Super Premium Brands, EVs.

Introduction

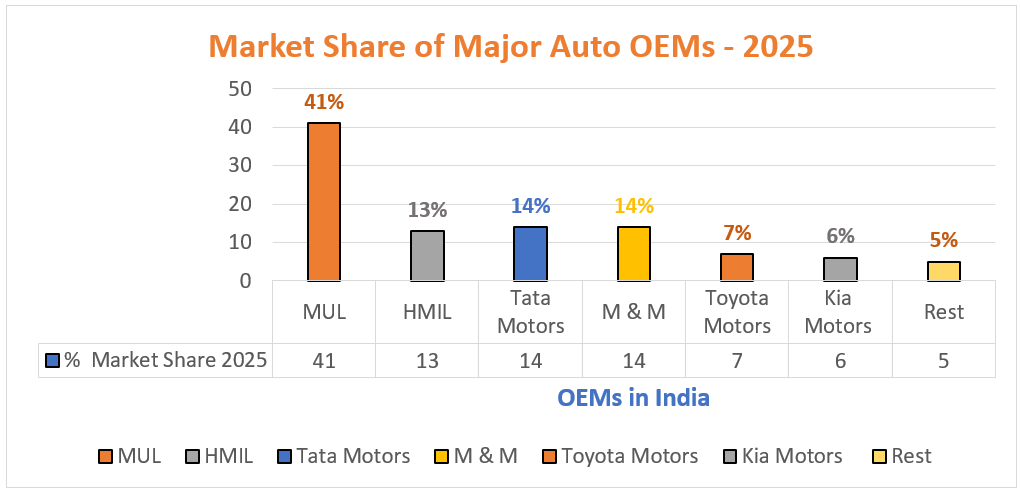

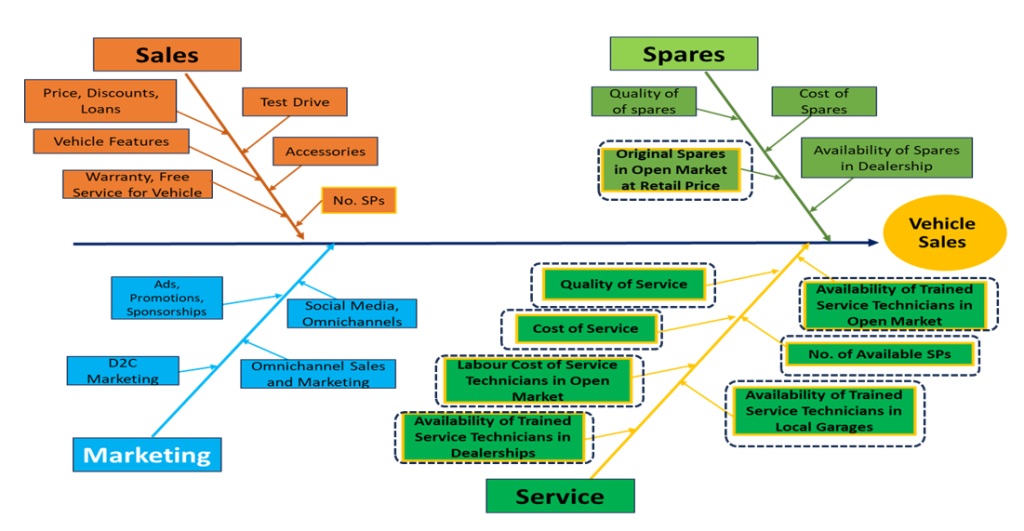

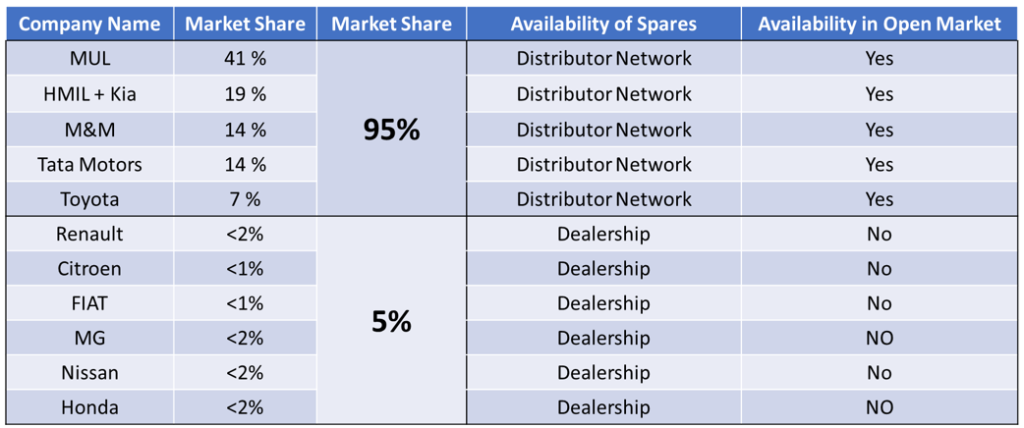

In the Automotive Industry, Expansion of a Product Line and Mass Acceptance of a Product are based on the Quality, Reliability, Durability, Affordability, Features and Service Points(Q-R-D-A-F-SP). A Good Product requires adequate Service Points to expand its reach in the market. In today’s competitive market, (Q-R-D-A-F) are the given expectations in a Brand. And the Market Dynamics have been able to pull the Product Quality of major brands to a threshold level to be reliable enough to compete with each other on the basis of Quality and Durability. Let us look into the market share of major OEMs:

So, why is it that 95% of the market is shared by 6 major Auto Brands, and a miniscule 5% is being contested by the rest of the brands? Some major brands, with average features, do very well, whereas some brands, with fully loaded features and technology, are not able to survive. Is it only Product Quality that decides the market share? Probably not, because if that were the case, then Honda/Toyota should have been commanding a larger market share!! Among all the factors like “Q-R-D-A-F-SP” that command a Market Share, the availability of Service Points is an important aspect. The Acceptability of the Product and its Dominance in the market need to be backed by adequate SP.

Few Case Studies:

Hyundai Motors India Ltd, when they started (1998-1999) they had ‘0 presence’ in India. They started with an Ad – ‘The Billion Dollar Car’. Leading newspapers, running ads every morning, created hype in readers’ minds who started the day with TOI, HT, The Hindu, etc. And finally, when Santro was launched, it had all the ingredients to lead the entry segment – Affordable 5 Seater Hatchback to accommodate a nuclear family.

Most of the starting Dealers from the Tata Motors Family were Well-trained and adequately sensitised to the need to hand-hold the Customer. The initial batches of Dealer Technicians and Dealer Workshop Managers were well trained; they were thoroughly pampered and were given elite treatment in the Induction Programme. When Customers came for enquiries, front line Managers and Technicians spoke volumes about the Company and the Product. Hyundai had an Aggressive Marketing Strategy and was always able to create a space in the minds of car lovers. Prospects were tracked, and the Sales Pipelines were meticulously closed. All these, buoyed by a customer-friendly approach, started creating an impact and acceptance in the customers’ perception of Hyundai! With the gradual expansion of dealer networks, Service Campaigns were introduced, and Customer Connect Initiatives were launched. And within a few years, HMIL had made successful inroads into the market.

HMIL had bold aspirations to grow. And it revolved around its philosophy of Employee Care. Employees were Recognized and Rewarded with Healthy Emoluments and Gifts. Employees used to eagerly wait for Gold Coins and the Annual Bonus every year. Since employees were well taken care of, the same aspirations translated into each and every employee of the organisation, who would speak volumes about HMIL. For the Sales and Service Teams, Weekly Dealer Visits were a must. Dealer Visits were framed more as an Incentive for the Employee than as a regular task. (Wayback in 2004-05, North East was infested with terrorism and militancy. However, an Adequate and a Protective Dealer Network in the North East, and HMIL’s flexibility to accommodate Travel Plans, employees were always willing to travel. HMIL started as a Marketing Driven Organisation, and its success centred around the Healthy HR Policies and Practices, which revolved around Employee Care. (Thanks to the lovely initiatives and forward-looking strategies of GS Ramesh Sir.) There was no looking back for HMIL since its inception in India.

FIAT India Ltd: They had started in India much ahead of others. And their flagship product, the FIAT Uno, was probably one of the best, ahead of others. Diesel Engine, Good Mileage, Sturdy Body, Comfortable RHBS, Reliable Technology, Dependable Quality – it had all the ingredients of a successful small car. The technology FIAT offered was as good, and sometimes ahead of, its competitors’. Then the question was, why did FIAT vanish from the Market? Inadequate Marketing and limited service points all across the country could be a few possible reasons! Secondly, co-selling under the banner of its competitors did not allow the FIAT Brand to evolve. A company with a Reliable and Superior Product Line effectively vanished from the Indian market!!

Understanding and Assumptions:

Assuming that a given OEM is able to maintain a healthy Product with “Q-R-D-A-F-SP”, why do some companies fail, in spite of having a good product line, and why do some companies make it to the finish line, in spite of having an average product!

The answer probably lies in:

- Product Marketing and Market Strategy

- Flexibility and Adaptability of the OEMs to Respond to Indian Business Conditions

Assuming that the Sales Demo and Product Demonstration have happened successfully, assuming that the customer has been able to satiate his/her product experience through a successful Test Drive, assuming that the sales agreement and discounts have been able to match customer expectations, Availability of Service Points is an important aspect that adds to the Saleability of the Product.

Post-sales Customer Ownership Patterns:

- Post Free Service, some cars never report back to Dealerships

- Post Warranty Period, some cars never visit Dealer SPs, and explore local garages and workshops

- Post-honeymoon period, car owners evaluate the Cost of Retention and Cost of Ownership of their vehicles.

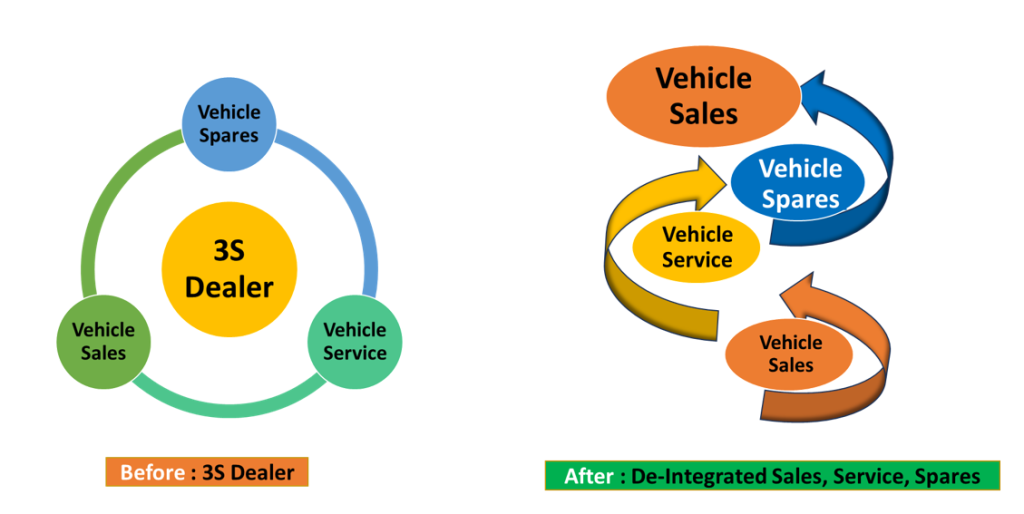

- 3S Business Model

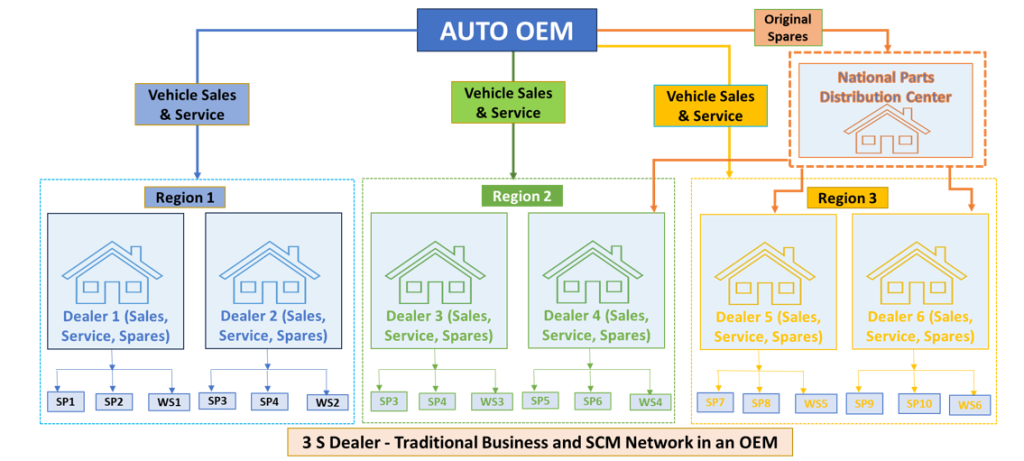

Below is the Traditional Automotive Business Model.

Closed Circuit Sales-Service-Spares Network

Most OEMs start 3S Dealer Networks as Sales-Service-Spares under a single roof (as shown in the above picture).

But there were Inherent Challenges with the 3S Models. When the OEM sought to diversify its SPs, an inherent dependence on the Vehicle Dealers for spares became apparent. The dealers saw a Business Threat in the individual SPs, coupled with the reluctance to pass on the Spares margin to the SPs. This created a bottleneck for the SPs to perform and grow. So, MUL, being the market leader, addressed the problem differently.

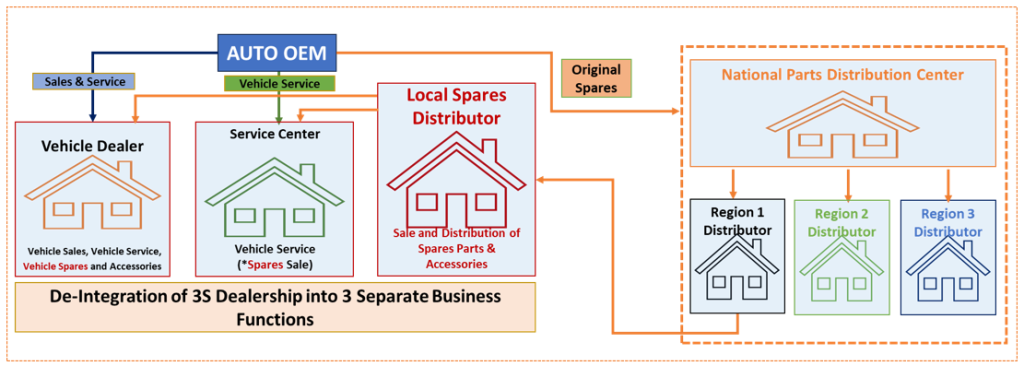

- MUL Business Model

Maruti is the 1st company to have started the MASS(Maruti Authorised Service Station). Started under the guidance of Dr K. Kumar, MUL’s focus was to multiply SPs. Qualified Garages and Workshops were identified, adequately equipped and trained, and onboarded into the MASS programme. And spares were distributed through the Regional Parts Distribution Network. For the 1st time, Service and Spares was separated as a separate Business Function. Service was taken to regular workshops. And spares were distributed through the Regional Parts Distribution Network.

Earlier, regular workshops and garages did not have the recognition and the authority to service Maruti Vehicles. Now, MASS had the authority to service Maruti Vehicles, and MASS workshops were also getting recognition for the same. This was adequately backed by independent Regional Parts Distributor Centres. This would not have been possible if spares had not been readily available to the Service Points.

3S Model was de-integrated and separated from each other under 03 different roofs: Sales, Service, and Spares.

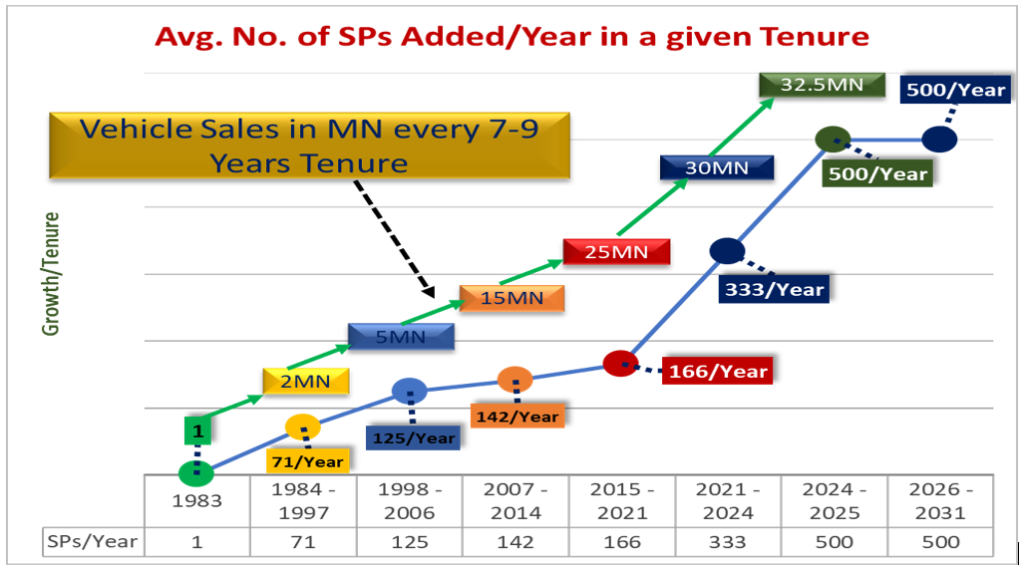

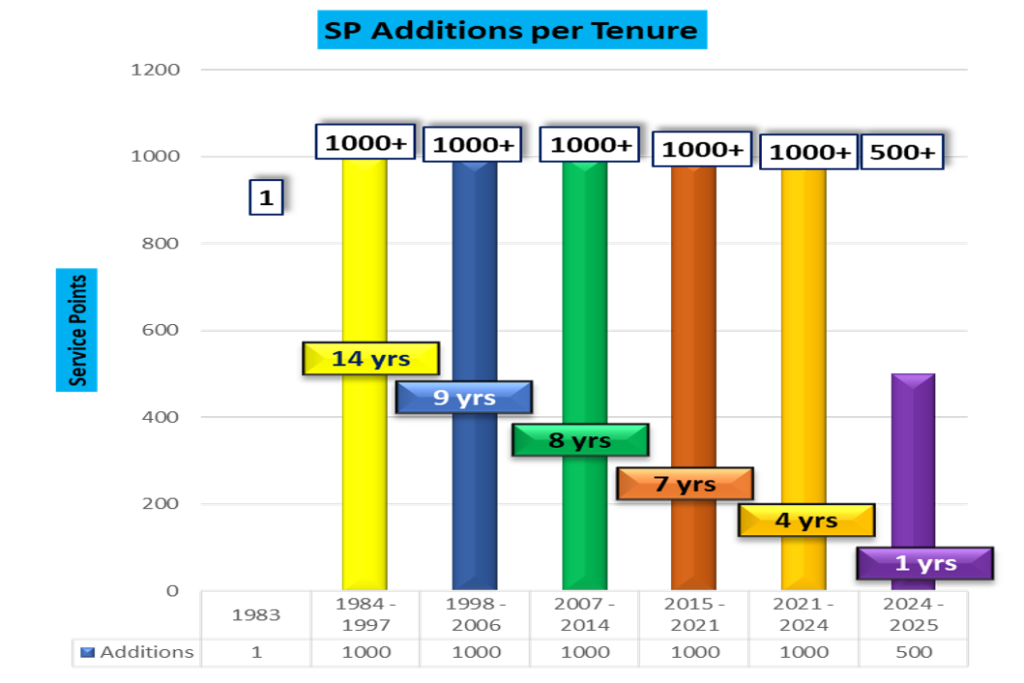

MUL Growth Story

Cause Or Effect – How the Market Forces Operate

The splitting of the 3S Dealer Model into individual Business Functions had a +ve Spiral effect on Business Growth. The Business Value that was locked into the 3S Business Model was unlocked by the Dynamic Market Forces. Sales – Service – Spares started functioning as Independent Market forces, entangled with each other, each responsible for the growth of the other.

The Game Changer

Is it the spares market only that drives Vehicle Sales? NO

Is it the availability of Service Points that decides Vehicle Sales? NO

Is it the Vehicle Dealership alone that is responsible for Vehicle Sales? NO

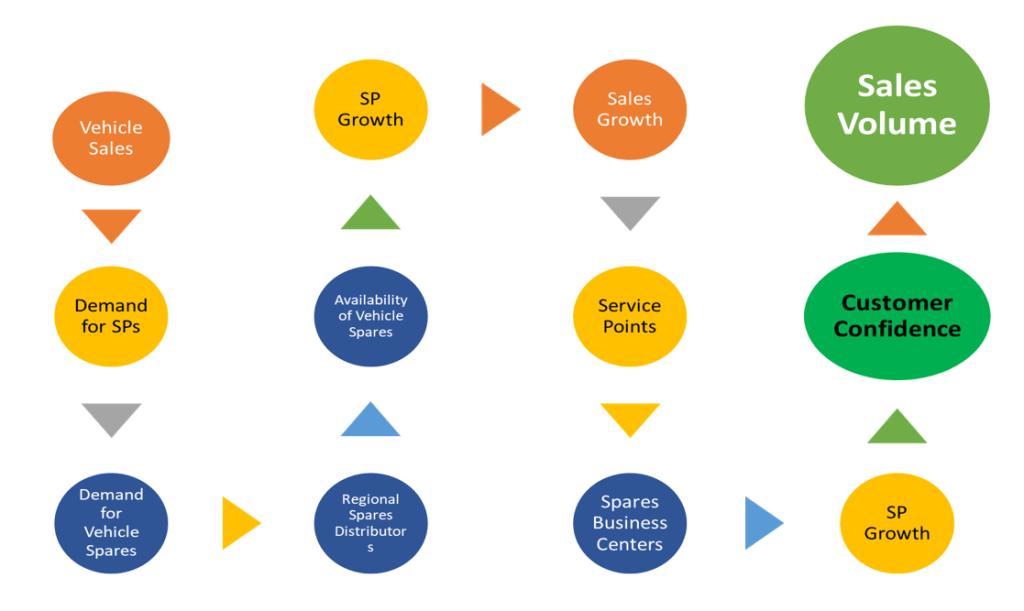

But independently, the 3-S forces together form an interlocking dependence and an interlocking integrated value chain with each other that directly impacts Vehicle Sales. The de-integrated 3-S forces are Value Locked Profit Centres that operate as Free Market Forces, each driving the growth of the other. With the increase in Vehicle Sales, the need for SPs increases. With the expansion and growth of SPs, the need for Easy Availability of spares increases. In such a Business Scenario, the availability of spares had to be liberated from the control and influence of the dealers. Once this was done, spares were easily available in the open market. As a result, Garage Technicians and Local Mechanics had the confidence to respond to every vehicle that came for repair. This confidence in the mechanics was translated into the customers’ confidence in the product.

The lifeline of the Automotive Industry is its after-sales support and service network. The availability of Original Spares (JIT!) acts like fresh Oxygen that feeds and runs this lifeline.

As vehicle volumes increased, demand for Vehicle Service Points rose. With the increase in Vehicle Service Points, the need for easy access to spares arose.

So, what has been the game-changer?! The availability of Original Spares in the open market has allowed and encouraged independent SPs to mushroom and grow. This growth has been translated into Customer Confidence in the product. The Customer Confidence created a Belief System in OEM. And that has translated into vehicle sales.

Some products with Superior “Q-R-D-A-F” have to contest within the 5% market share!!

Takeaways:

- 3S -> 1S + 1S + 1S: For a non-premium Automotive brand, the dynamics of growth lie in de-integrating Sales, Service and Spares under 3 Separate Business Roofs. And allow them to operate as Independent Market Forces.

- Customer Confidence in a product grows with the multiplication of Service Points and Service Network availability (X Authorised Service Stations). TPASS (Third Party Authorised Service Stations) is an easy, time-proven solution that fuels Customer Confidence and Sales Growth.

- Service Champion Programme: OEMs should identify, adopt, and integrate Roadside Mechanics and Local Garage Technicians into a structured programme that allows them to operate as Brand Ambassadors as X Certified Service Champions (XCSP).

- Ease of Availability of Original Spare Parts in the Open Market through Dedicated Distributor Channels will Fuel Vehicle Sales Growth (and keep spurious parts away from the 2nd Sales Market).

Acknowledgements:

1. Local auto garages, Local automotive workshops, Roadside Mechanics and Technicians

2. Dealer Technicians, Dealer Workshops

3. Local Auto Parts Stockists, Distributors, Scrap Dealers, 2nd sales market operators

4. Senior Business Leaders in SCM and IT, Auto Industry Business Leaders, Auto Industry Veterans

5. HoDs of Premiere Technical Research Institutes

6. Just-in-Time (JIT) Mechanism for easy availability of Original Spare Parts in the Open Market

Disclaimer:

1. Some OEMs have a policy of making spares available only at the Dealership. The author honours the company policy and has no Intent to challenge or influence the Company Policy.

2. Data Source: All the data shared in the document has been obtained from Google Search, Copilot AI, Perplexity AI, SIAM, Press Releases and Local Spare Distributors. (Fluctuations of a few %age, numbers in the data source may be possible due to a fiercely Dynamic and a Competitive Auto Market.)

3. The intent of the Article has been to identify the market forces that are responsible for the growth of vehicle sales and help the OEMs grow by taking advantage of this Learning.

About the Author

Bhaskar Nandi

He is an ex-Hyundai, ex-Honda, ex-Mahindra & Mahindra, and ex-IFB Industries employee, currently working as a Consultant in a Global IT Company. He carries 27+ years of experience.

Also read: India’s Electric Vehicle Market: 2.3 million units and counting- CY 2025 annual insights

Subscribe & Stay Informed

Subscribe today for free and stay on top of latest developments in EV domain.