Sodium-ion batteries | Current status of the technology and supply chain

Recently, sodium-ion batteries have garnered significant attention as a potential alternative to lithium-ion batteries. With global giants like CATL and BYD investing in the technology and promising large-scale production, the prospects of sodium-ion batteries have captured the interest of the energy storage and automotive industry. Dr Yashodan Gokhale, CTO – Battrixx, discusses the current status of sodium ion technology, supply chain dynamics, and challenges that need to be overcome to make it a commercial reality.

Advantages of Sodium-ion battery technology

Sodium-ion batteries offer several advantages over lithium-ion batteries, including improved performance at lower temperatures and a reduced supply chain dependency. The sodium-ion battery offers a significant advantage in cold temperature storage, as it performs remarkably well even at extremely low temperatures, such as -10°C or -20°C. Sodium-ion batteries have the advantage of high power capabilities, enabling their use in both power and energy applications, with the potential to operate at 3C or 4C high-power rates. One of the significant advantages of sodium-ion batteries is their safety profile. The ability to withstand extreme temperatures and humidity levels further enhances their appeal.

Technology readiness and commercial usage

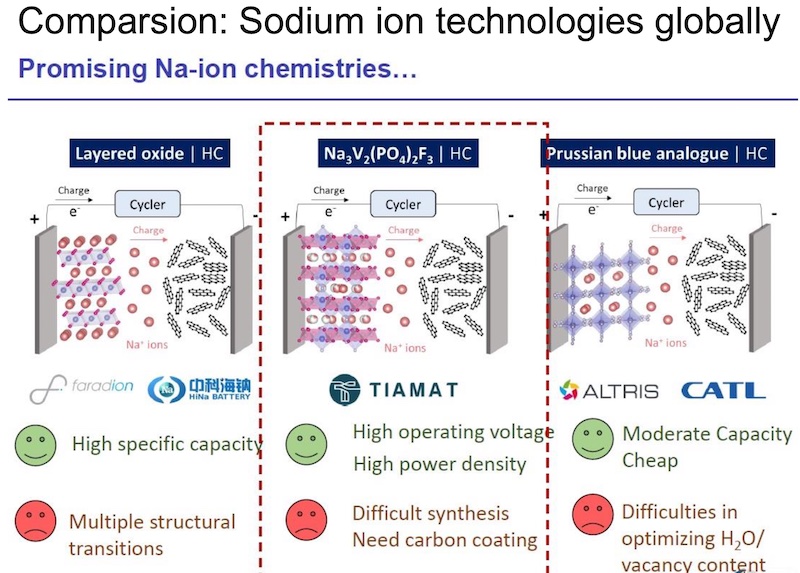

Furthermore, numerous players in the industry are making bold claims about its long cycle life, boasting about achieving more than 4,000 to 5,000 cycles. Moreover, achieving the desired performance and cycle life comparable to lithium-ion batteries remains a focal point for further development. Many companies, such as Faradion, Tiamat (Europe), CATL (China), BYD, HINA, KPIT, NCL, and IIT Roorkee, are actively involved in sodium ion research and development.

Sodium-ion Battery Company List

– Faradion Limited

– AMTE Power PLC

– NGK Insulators Ltd

– HiNa Battery Technology Co. Ltd

– TIAMAT SAS

– Contemporary Amperex Technology Co. Limited.-CATL

– Altris AB

– Natron Energy Inc.

– Altris

– BYD

While some companies have announced advancements in their products, most are still in the technology readiness levels (TRL) between 5 and 6, which means they are showing promising results but have not reached the level required for commercial production (TRL 7-9). The choice of cathode and anode materials is a critical aspect that varies between companies and may impact the overall commercial readiness of the technology. While some companies have demonstrated promising results and even showcased vehicles powered by sodium-ion batteries, commercial accessibility is still some years away. Major players like CATL, HINA, and BYD have showcased their progress with sodium-ion battery technology, e.g. JAC Group announced a vehicle launch in collaboration with HiNa batteries. However, practical availability is still limited for original equipment manufacturers (OEMs) or companies interested in purchasing sodium-ion cells to build battery packs. It is projected that by the first or second quarter of 2024, OEMs may be able to buy the cells and create battery packs, similar to the process with readily available lithium-ion cells, after going through necessary certifications.

Despite the media hype about sodium-ion batteries being a game-changer, there are some important drawbacks that need to be addressed. Energy densities in sodium-ion batteries are currently in the range of 100 wh/kg to 160 wh/kg, which can match the performance of LFP (Lithium Iron Phosphate) batteries. However, achieving reproducibility and scalability to meet large-scale demand, such as producing one million sodium-ion cells for a specific region like India, is still challenging. Research involves experimenting with various elements from the periodic table and selecting the right materials to achieve the desired performance, such as matching the wh per kg of LFP batteries.

Cost and energy density challenges

Cost is another significant factor hindering the commercial adoption of sodium-ion batteries. Although the industry aims to match the price of sodium-ion batteries to lead-acid batteries by 2025 or 2026, the current cost is relatively high, comparable to NMC (Nickel Manganese Cobalt) batteries or even higher. The raw material used in sodium-ion batteries impacts the cost, and ongoing research and development efforts in anode and electrolyte technologies are expected to bring down the cost over time gradually.

Major companies like CATL, BYD, Panasonic, Samsung, LG, and others have invested billions of dollars in developing their supply chains and reducing costs, making it challenging for sodium-ion batteries to compete in terms of price initially. While sodium-ion batteries hold promise for the future, their practical availability, reproducibility, and cost-effectiveness still require further developments and optimization. While LFP batteries have a proven track record, sodium-ion batteries offer the potential for higher energy densities, exceeding 200 wh per kg, which makes them appealing for various applications. As the technology evolves and progresses, we can expect sodium-ion batteries to become more accessible and cost-competitive, making them a viable option for various applications in the energy storage and transportation sectors.

Supply chain and equipment

In the context of securing the supply chain for cell manufacturing, Indian companies are learning from the global platform and realizing the importance of controlling the supply chain to reduce costs and ensure good quality. Major Indian OEMs and cell manufacturers, some of whom are part of the PLI (Production Linked Incentive) scheme, are actively monitoring their supply chains. By strategically partnering with mining and refining companies, they aim to secure the necessary raw materials for cell production, similar to how Tesla collaborated with Panasonic to control the sourcing of graphite, cobalt, and nickel for their batteries.

To establish a robust supply chain for sodium-ion batteries, the main challenges lie in sourcing critical materials and maintaining quality. The challenge of hard carbon, a key material used in sodium-ion batteries, is being addressed by European and Japanese companies and some Indian groups who are working on producing high-quality hard carbon. Ensuring the purity and quality of these materials is essential to avoid issues with expansion and dendrite formation during cell reactions, especially in regions with varying temperatures like India.

The supply chain for sodium-ion batteries is not as well-established at the moment. The lithium-ion supply chain is more mature and easier to access, with several Indian companies already making significant investments in lithium-ion gigafactories. On the other hand, sodium-ion batteries are still in the prototyping and demonstration phase, and gigafactories for sodium-ion cells are expected to start running in neighbouring countries by the end of 2024.

Regarding equipment manufacturing, there is a high demand for machinery to set up fully automatic production lines for battery cells. Indian companies are building or importing machinery from various countries to support the growth of lithium-ion gigafactories. As the demand for sodium-ion batteries increases, similar efforts will be made to establish equipment manufacturing for sodium-ion cells in India. By around 2025, it is anticipated that the installation of equipment for sodium-ion batteries will be in progress, enabling the stepwise growth of the market share for sodium-ion technology in India.

Electrolytes and separators

The supply chain for electrolytes and separators for sodium-ion batteries is gradually maturing, and by the end of this year, the production of electrolytes is expected to begin outside India, with eventual expansion to India’s production capabilities.

Challenges for replacing lithium-ion with sodium-ion batteries

For sodium-ion batteries to replace lithium-ion batteries in various applications, industry players need to address the following challenges:

Developing economical sodium-ion cells: Sodium ion cells must become cost-competitive with lithium-ion cells to encourage widespread adoption. For example, in the case of electric two-wheelers and three-wheelers, cost and range are critical factors. Manufacturers aim to offer cost-effective vehicles with longer single-charge range as customers prioritize these aspects.

Addressing energy density: The industry must assess the specific applications and requirements. Improving energy density to match or exceed lithium iron phosphate batteries is crucial for gaining traction in the market.

Volume production and accessibility: Companies need to scale up production and ensure accessibility for OEMs to integrate sodium-ion batteries into their products.

Overcoming technological barriers: Challenges related to hard carbon anodes, expansion issues, and other manufacturing complexities must be resolved.

Ensuring safety: This is another crucial aspect. Safety standards have been a concern in the unorganised electric vehicle manufacturing sector. Sodium-ion batteries can improve safety since they are less prone to thermal events compared to high-energy dense lithium-ion batteries. This can be especially beneficial in regions with extreme temperatures, as sodium-ion batteries offer better thermal stability.

Conclusion

Sodium-ion batteries show immense promise as a viable alternative to lithium-ion batteries. While significant progress has been made in their development, commercial accessibility and cost-competitiveness remain critical milestones to achieve. With ongoing research and industry collaborations, sodium-ion technology is expected to mature further, eventually establishing itself as a reliable and sustainable energy storage solution for the future.

Also Read: Sodium-ion batteries| An alternative to Li-ion batteries?

Subscribe & Stay Informed

Subscribe today for free and stay on top of latest developments in EV domain.

sodium ion is the near future and Lithium will slow down gradually mainly abundant available resources comparison wilt lithium the prices are going to drop drastically. any new invention has challanges it should overcome over a period of time.

This article contains false information. The production cost of sodium ion batteries is less than that of lithium ion batteries by nearly 20%, this is mostly due to mining and transportation costs. The cost is not a hurdle, the change will only be costly for corporations losing lithium investments. There’s also significant information missing from this: China already shifted part of their power storage infrastructure to sodium-ion. This isn’t even new technology, we’ve had the ability to make sodium-ion batteries for decades but didn’t because everyone thought lithium tech would surpass it. Also despite the fact that sodium-ion batteries are less energy dense, they transfer energy with less bleed off in the forms of heat and vibration than lithium ion batteries, ultimately making them the more energy efficient option. The only thing preventing their commercial availability currently is that corporations have sunk billions into lithium and don’t want to now invest in the switch. Which makes even more sense when you go digging and find that companies like Duracell have stakes in lithium mines and will lose a lot of money in the switch over to sodium. It’s also unacceptable that you’d write this article and not bring up the rampant slavery in the lithium mining industry. If you own a lithium battery, odds are good a slave handled it at some point.

All in all, this article reads like blatant propaganda to anyone that is educated on this topic:

https://evreporter.com/sodium-ion-batteries-current-status-of-the-technology-and-supply-chain/

Pingback: KPIT unveils Sodium-ion battery technology | Invites partners to commercialise the tech • EVreporter

Pingback: Sodion Energy introduces its Sodium-ion batteries | Energy density up to 140 Wh/kg • EVreporter

Pingback: Sodium-ion batteries: A real challenger or another passerby for Indian storage tech? • EVreporter